- Country United States

- Other

- Followed by 49 people

Recent Updates

- 𝙀𝙣𝙚𝙧𝙜𝙞𝙯𝙚 𝙔𝙤𝙪𝙧 𝙄𝙣𝙫𝙚𝙨𝙩𝙢𝙚𝙣𝙩𝙨 - 𝙐𝙣𝙡𝙚𝙖𝙨𝙝𝙞𝙣𝙜 𝙋𝙤𝙩𝙚𝙣𝙩𝙞𝙖𝙡 𝙋𝙧𝙤𝙛𝙞𝙩𝙨 𝙞𝙣 𝙩𝙝𝙚 𝘽𝙤𝙤𝙢𝙞𝙣𝙜 𝙁𝙡𝙤𝙬 𝘽𝙖𝙩𝙩𝙚𝙧𝙮 𝙈𝙖𝙧𝙠𝙚𝙩

‘Flow Battery Market by Type (redox flow battery, hybrid flow battery), Material (zinc-bromine, vanadium, hydrogen-bromine), Ownership, Application (utilities, commercial & industrial), and Geography - Global Forecast to 2030.

Download Free Sample Report Here : https://www.meticulousresearch.com/download-sample-report/cp_id=5419

According to the latest publication from Meticulous Research®, the flow battery market is projected to reach $885.3 million by 2030, at a CAGR of 17% during the forecast period of 2023 to 2030. The growth of this market is driven by the high demand for flow battery for utility applications and the increasing investments in renewable energy. However, the lack of standardization for the development of flow battery systems and the high initial costs of manufacturing flow battery restrain the growth of this market.

Furthermore, technological innovations with improved capabilities are expected to create significant growth opportunities for the players operating in this market. However, the decline in the deployment rate of flow battery and the supply chain disruption of raw materials for battery manufacturing pose challenges to the market’s growth.

The flow battery market is segmented based on type, material, ownership, application, and geography.

Based on type, the flow battery market is segmented into redox flow battery and hybrid flow battery. In 2022, the redox flow battery segment accounted for the larger share of the flow battery market. Redox flow battery are economical and convenient sources of storing electrical energy at a grid scale and for various applications, which contributes to the large market share of this segment.

Based on material, the flow battery market is segmented into zinc-bromine, vanadium, hydrogen-bromine, polysulfide bromine, and other materials. In 2022, the zinc-bromine segment accounted for the largest share of the flow battery market. The large market share of this segment is attributed to the benefits offered by zinc-bromine flow battery, including relatively high energy density, deep discharge capability, and good reversibility.

Based on ownership, the flow battery market is segmented into customer-owned, third-party-owned, and utility-owned. In 2022, the utility-owned segment accounted for the largest share of the flow battery market. The large market share of this segment is attributed to the increasing electrification initiatives by various governments and stakeholders to power distant and remote locations.

Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5419

Based on application, the flow battery market is segmented into utilities, commercial & industrial, EV charging stations, off-grid & micro-grid power, and other applications. In 2022, the utilities segment accounted for the largest share of the flow battery market. The adoption of flow battery is increasing in utilities due to the growing need for electrification. Furthermore, the growing use of renewable energy across grids has increased the demand for efficient, flexible, and long-lasting energy storage solutions.

Based on geography, in 2022, Asia-Pacific (APAC) accounted for the largest share of the flow battery market. Asia-Pacific’s major market share is attributed to the increasing demand for flow battery from countries such as Japan and Australia. In addition, the growing adoption of energy storage solutions for industrial, utilities, and other applications and the rising demand for flow battery for grid and microgrid applications contributes to the growth of this regional market.

Key Players:

The major players operating in this market are Invinity Energy Systems PLC (Europe), ESS Inc. (U.S.), Primus Power Corporation (U.S.), ViZn Energy Systems (U.S.), EnSync Energy Systems (U.S.), Sumitomo Electric Industries, Ltd. (Japan), UniEnergy Technologies, LLC (U.S), Dalian Rongke Power Co. Ltd. (China), Redflow Limited (Australia), Elestor BV (Netherlands), Enerox GmbH (Austria), Largo Inc. (U.S.), RFC Power Ltd (Europe), H2, Inc. (South Korea), CellCube Energy Storage Systems Inc. (U.S.), Voltstorage GmbH (Germany), Vanadis Power GmbH (Germany), and LE SYSTEM CO., Ltd (Japan).

To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/flow-battery-market-5419

Key questions answered in the report:

Which are the high-growth market segments in terms of type and application?

What was the historical market size for flow battery?

What are the market forecasts and estimates for the period 2023–2030?

What are the major drivers, restraints, opportunities, and challenges in the global flow battery market?

Who are the major players in the flow battery market, and what are their market shares?

How is the competitive landscape in the global flow battery market?

What are the recent developments in the global flow battery market?

What are the different strategies adopted by the major players in the global flow battery market?

What are the key geographic trends, and which are the high-growth countries?

Quick Buy – https://www.meticulousresearch.com/Checkout/46850397

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

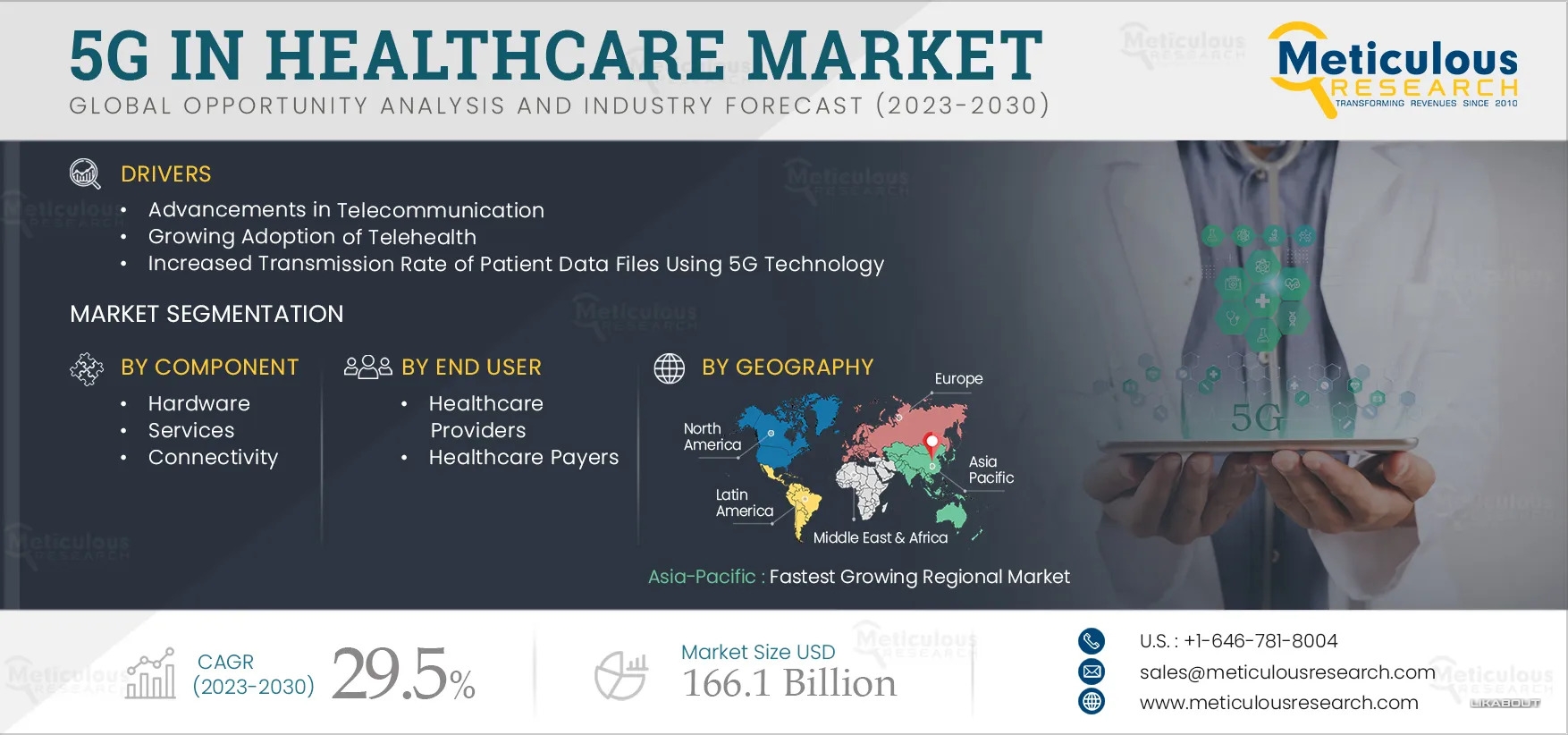

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research𝙀𝙣𝙚𝙧𝙜𝙞𝙯𝙚 𝙔𝙤𝙪𝙧 𝙄𝙣𝙫𝙚𝙨𝙩𝙢𝙚𝙣𝙩𝙨 - 𝙐𝙣𝙡𝙚𝙖𝙨𝙝𝙞𝙣𝙜 𝙋𝙤𝙩𝙚𝙣𝙩𝙞𝙖𝙡 𝙋𝙧𝙤𝙛𝙞𝙩𝙨 𝙞𝙣 𝙩𝙝𝙚 𝘽𝙤𝙤𝙢𝙞𝙣𝙜 𝙁𝙡𝙤𝙬 𝘽𝙖𝙩𝙩𝙚𝙧𝙮 𝙈𝙖𝙧𝙠𝙚𝙩 ‘Flow Battery Market by Type (redox flow battery, hybrid flow battery), Material (zinc-bromine, vanadium, hydrogen-bromine), Ownership, Application (utilities, commercial & industrial), and Geography - Global Forecast to 2030. Download Free Sample Report Here : https://www.meticulousresearch.com/download-sample-report/cp_id=5419 According to the latest publication from Meticulous Research®, the flow battery market is projected to reach $885.3 million by 2030, at a CAGR of 17% during the forecast period of 2023 to 2030. The growth of this market is driven by the high demand for flow battery for utility applications and the increasing investments in renewable energy. However, the lack of standardization for the development of flow battery systems and the high initial costs of manufacturing flow battery restrain the growth of this market. Furthermore, technological innovations with improved capabilities are expected to create significant growth opportunities for the players operating in this market. However, the decline in the deployment rate of flow battery and the supply chain disruption of raw materials for battery manufacturing pose challenges to the market’s growth. The flow battery market is segmented based on type, material, ownership, application, and geography. Based on type, the flow battery market is segmented into redox flow battery and hybrid flow battery. In 2022, the redox flow battery segment accounted for the larger share of the flow battery market. Redox flow battery are economical and convenient sources of storing electrical energy at a grid scale and for various applications, which contributes to the large market share of this segment. Based on material, the flow battery market is segmented into zinc-bromine, vanadium, hydrogen-bromine, polysulfide bromine, and other materials. In 2022, the zinc-bromine segment accounted for the largest share of the flow battery market. The large market share of this segment is attributed to the benefits offered by zinc-bromine flow battery, including relatively high energy density, deep discharge capability, and good reversibility. Based on ownership, the flow battery market is segmented into customer-owned, third-party-owned, and utility-owned. In 2022, the utility-owned segment accounted for the largest share of the flow battery market. The large market share of this segment is attributed to the increasing electrification initiatives by various governments and stakeholders to power distant and remote locations. Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5419 Based on application, the flow battery market is segmented into utilities, commercial & industrial, EV charging stations, off-grid & micro-grid power, and other applications. In 2022, the utilities segment accounted for the largest share of the flow battery market. The adoption of flow battery is increasing in utilities due to the growing need for electrification. Furthermore, the growing use of renewable energy across grids has increased the demand for efficient, flexible, and long-lasting energy storage solutions. Based on geography, in 2022, Asia-Pacific (APAC) accounted for the largest share of the flow battery market. Asia-Pacific’s major market share is attributed to the increasing demand for flow battery from countries such as Japan and Australia. In addition, the growing adoption of energy storage solutions for industrial, utilities, and other applications and the rising demand for flow battery for grid and microgrid applications contributes to the growth of this regional market. Key Players: The major players operating in this market are Invinity Energy Systems PLC (Europe), ESS Inc. (U.S.), Primus Power Corporation (U.S.), ViZn Energy Systems (U.S.), EnSync Energy Systems (U.S.), Sumitomo Electric Industries, Ltd. (Japan), UniEnergy Technologies, LLC (U.S), Dalian Rongke Power Co. Ltd. (China), Redflow Limited (Australia), Elestor BV (Netherlands), Enerox GmbH (Austria), Largo Inc. (U.S.), RFC Power Ltd (Europe), H2, Inc. (South Korea), CellCube Energy Storage Systems Inc. (U.S.), Voltstorage GmbH (Germany), Vanadis Power GmbH (Germany), and LE SYSTEM CO., Ltd (Japan). To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/flow-battery-market-5419 Key questions answered in the report: Which are the high-growth market segments in terms of type and application? What was the historical market size for flow battery? What are the market forecasts and estimates for the period 2023–2030? What are the major drivers, restraints, opportunities, and challenges in the global flow battery market? Who are the major players in the flow battery market, and what are their market shares? How is the competitive landscape in the global flow battery market? What are the recent developments in the global flow battery market? What are the different strategies adopted by the major players in the global flow battery market? What are the key geographic trends, and which are the high-growth countries? Quick Buy – https://www.meticulousresearch.com/Checkout/46850397 Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research0 Comments 0 Shares11 - 𝑭𝒂𝒔𝒕, 𝑺𝒆𝒄𝒖𝒓𝒆, 𝒂𝒏𝒅 𝑬𝒇𝒇𝒊𝒄𝒊𝒆𝒏𝒕 -𝑼𝒏𝒍𝒆𝒂𝒔𝒉𝒊𝒏𝒈 𝒕𝒉𝒆 𝑷𝒐𝒘𝒆𝒓 𝒐𝒇 5𝑮 𝒊𝒏 𝑯𝒆𝒂𝒍𝒕𝒉𝒄𝒂𝒓𝒆

Meticulous Research®—a leading global market research company, published a research report titled ‘5G in Healthcare Market by Component (Hardware, Services [Professional, Managed], Connectivity), Application (Healthcare Management, Remote Healthcare, AR/VR, Asset Tracking, Connected Medical Devices), End User (Payer, Provider) - Global Forecast to 2030.'

Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5431

According to this latest publication from Meticulous Research®, the 5G in healthcare market is projected to reach $166.1 billion by 2030, at a CAGR of 29.5% during the forecast period. The growth of this market is attributed to factors such as the advancements in telecommunication, the increased patient data transmission rate offered by 5G technology, the increasing adoption of telehealth and nursing robots after the COVID-19 outbreak, the availability of low-cost sensors, and the increasing adoption of 5G-enabled medical devices for patient monitoring.

5G in Healthcare Market: Future Outlook

The 5G in healthcare market is segmented based on Component (Hardware, Services [Professional Services, Managed Services], Connectivity), Application (Healthcare Management Software, Remote Healthcare [Remote Patient Monitoring, Virtual Consultations, Video-Enabled Prescription Management], Augmented Reality/Virtual Reality, Asset Tracking for Medical Devices, Connected Medical Devices, Other Applications), End User (Healthcare Providers, Healthcare Payers, Other End Users), and Geography. The study also evaluates industry competitors and analyzes the market at the regional and country levels.

Based on component, in 2023, the hardware segment is expected to account for the largest share of the 5G in healthcare market. The growth of this segment is attributed to the need for upgrading devices for optimal use of the latest technologies, the rising demand for ultra-high bandwidth for connecting devices, and the need for massive connectivity.

Based on application, the 5G in healthcare market is segmented into healthcare management software, remote healthcare, augmented reality (AR)/virtual reality (VR) healthcare, telemedicine, medical/nursing telerobotics, connected medical devices, and other applications. The remote healthcare segment is slated to register the highest CAGR during the forecast period. The growth of this segment is attributed to the growing need for long-term home care, the increasing burden of chronic diseases, the rising geriatric population, and the growing demand for remote health checkups. Additionally, the rising awareness and demand for telehealth consultations drive the demand for remote patient monitoring solutions.

Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5431

Geographic Review:

This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S. and Canada), Europe (Germany, France, U.K., Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa.

In 2023, North America is expected to account for the largest share of the 5G in healthcare market, followed by Europe and Asia-Pacific. Furthermore, the U.S. is expected to be the largest shareholding market in North America in 2023. The market growth in the U.S. is attributed to the high disposable incomes of the population, the rising number of patients with chronic diseases, favorable government investments for the digitalization of the healthcare sector, and the availability of advanced infrastructure for the implementation of 5G services.

Key Players:

The key players operating in the 5G in healthcare market are AT&T Inc. (U.S.), Verizon Communications Inc. (U.S.), LM ERICSSON TELEPHONE COMPANY (Sweden), T‑Mobile USA, Inc. (U.S.), Cisco Systems, Inc. (U.S.), TELUS Corporation (U.S.), Telit corporate group (U.S.), Orange SA (France), Telefónica, S.A.(Spain), SAMSUNG ELECTRONICS CO., LTD. (South Korea), BT Group plc (U.K.), NEC Corporation (Japan), and QUALCOMM Incorporated (U.S.).

To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/5G-in-healthcare-market-5431

Key questions answered in the report-

Which are the high-growth market segments in terms of component, application, end user, and region/country?

What was the historical market size for 5G in healthcare across the globe?

What are the market forecasts and estimates for the period 2023–2030?

What are the major drivers, restraints, challenges, opportunities, and trends in the global market of 5G in healthcare?

Who are the major players in the global 5G in healthcare market?

How is the competitive landscape, and who are the market leaders in the global 5G in healthcare market?

What are the recent developments in the 5G in healthcare market?

What are the different strategies adopted by the major players in the 5G in healthcare market?

What are the geographical trends and high growth regions/countries?

Quick Buy- https://www.meticulousresearch.com/Checkout/76879625

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research𝑭𝒂𝒔𝒕, 𝑺𝒆𝒄𝒖𝒓𝒆, 𝒂𝒏𝒅 𝑬𝒇𝒇𝒊𝒄𝒊𝒆𝒏𝒕 -𝑼𝒏𝒍𝒆𝒂𝒔𝒉𝒊𝒏𝒈 𝒕𝒉𝒆 𝑷𝒐𝒘𝒆𝒓 𝒐𝒇 5𝑮 𝒊𝒏 𝑯𝒆𝒂𝒍𝒕𝒉𝒄𝒂𝒓𝒆 Meticulous Research®—a leading global market research company, published a research report titled ‘5G in Healthcare Market by Component (Hardware, Services [Professional, Managed], Connectivity), Application (Healthcare Management, Remote Healthcare, AR/VR, Asset Tracking, Connected Medical Devices), End User (Payer, Provider) - Global Forecast to 2030.' Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5431 According to this latest publication from Meticulous Research®, the 5G in healthcare market is projected to reach $166.1 billion by 2030, at a CAGR of 29.5% during the forecast period. The growth of this market is attributed to factors such as the advancements in telecommunication, the increased patient data transmission rate offered by 5G technology, the increasing adoption of telehealth and nursing robots after the COVID-19 outbreak, the availability of low-cost sensors, and the increasing adoption of 5G-enabled medical devices for patient monitoring. 5G in Healthcare Market: Future Outlook The 5G in healthcare market is segmented based on Component (Hardware, Services [Professional Services, Managed Services], Connectivity), Application (Healthcare Management Software, Remote Healthcare [Remote Patient Monitoring, Virtual Consultations, Video-Enabled Prescription Management], Augmented Reality/Virtual Reality, Asset Tracking for Medical Devices, Connected Medical Devices, Other Applications), End User (Healthcare Providers, Healthcare Payers, Other End Users), and Geography. The study also evaluates industry competitors and analyzes the market at the regional and country levels. Based on component, in 2023, the hardware segment is expected to account for the largest share of the 5G in healthcare market. The growth of this segment is attributed to the need for upgrading devices for optimal use of the latest technologies, the rising demand for ultra-high bandwidth for connecting devices, and the need for massive connectivity. Based on application, the 5G in healthcare market is segmented into healthcare management software, remote healthcare, augmented reality (AR)/virtual reality (VR) healthcare, telemedicine, medical/nursing telerobotics, connected medical devices, and other applications. The remote healthcare segment is slated to register the highest CAGR during the forecast period. The growth of this segment is attributed to the growing need for long-term home care, the increasing burden of chronic diseases, the rising geriatric population, and the growing demand for remote health checkups. Additionally, the rising awareness and demand for telehealth consultations drive the demand for remote patient monitoring solutions. Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5431 Geographic Review: This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S. and Canada), Europe (Germany, France, U.K., Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa. In 2023, North America is expected to account for the largest share of the 5G in healthcare market, followed by Europe and Asia-Pacific. Furthermore, the U.S. is expected to be the largest shareholding market in North America in 2023. The market growth in the U.S. is attributed to the high disposable incomes of the population, the rising number of patients with chronic diseases, favorable government investments for the digitalization of the healthcare sector, and the availability of advanced infrastructure for the implementation of 5G services. Key Players: The key players operating in the 5G in healthcare market are AT&T Inc. (U.S.), Verizon Communications Inc. (U.S.), LM ERICSSON TELEPHONE COMPANY (Sweden), T‑Mobile USA, Inc. (U.S.), Cisco Systems, Inc. (U.S.), TELUS Corporation (U.S.), Telit corporate group (U.S.), Orange SA (France), Telefónica, S.A.(Spain), SAMSUNG ELECTRONICS CO., LTD. (South Korea), BT Group plc (U.K.), NEC Corporation (Japan), and QUALCOMM Incorporated (U.S.). To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/5G-in-healthcare-market-5431 Key questions answered in the report- Which are the high-growth market segments in terms of component, application, end user, and region/country? What was the historical market size for 5G in healthcare across the globe? What are the market forecasts and estimates for the period 2023–2030? What are the major drivers, restraints, challenges, opportunities, and trends in the global market of 5G in healthcare? Who are the major players in the global 5G in healthcare market? How is the competitive landscape, and who are the market leaders in the global 5G in healthcare market? What are the recent developments in the 5G in healthcare market? What are the different strategies adopted by the major players in the 5G in healthcare market? What are the geographical trends and high growth regions/countries? Quick Buy- https://www.meticulousresearch.com/Checkout/76879625 Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research 0 Comments 0 Shares11

0 Comments 0 Shares11 - 𝑹𝒆𝒗𝒐𝒍𝒖𝒕𝒊𝒐𝒏𝒊𝒛𝒊𝒏𝒈 𝑬𝒚𝒆 𝑪𝒂𝒓𝒆: 𝑻𝒉𝒆 𝑫𝒚𝒏𝒂𝒎𝒊𝒄 𝑳𝒂𝒏𝒅𝒔𝒄𝒂𝒑𝒆 𝒐𝒇 𝑶𝒑𝒕𝒐𝒎𝒆𝒕𝒓𝒚 𝑬𝒒𝒖𝒊𝒑𝒎𝒆𝒏𝒕 𝑴𝒂𝒓𝒌𝒆𝒕

Meticulous Research®—a leading global market research company, published a research report titled ‘Optometry Equipment Market by Product (OCT Scan, Perimeter, Fundus Camera, Retinoscope, Keratometer, Ophthalmic Ultrasound, Tonometer, Slit Lamp, Chart Projector), Application (Cataract, Glaucoma, AMD), End User (Clinic, Hospital) - Global Forecast to 2029.’

Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5406

According to this latest publication from Meticulous Research®, the global optometry equipment market is projected to reach $5.4 billion by 2029, at a CAGR of 4% during the forecast period. The increasing cases of eye diseases and disorders, rising geriatric population, excessive use of laptops & mobile phones leading to visual impairments, and rising government initiatives and funding to improve access to eye care services are the factors driving the growth of this market.

Optometry Equipment Market: Future Outlook

The global optometry equipment market is segmented by Product Type (Retina & Glaucoma Examination Products [OCT Scanners, Perimeters, Fundus Cameras, Retinoscopes, Ophthalmoscopes, Ophthalmic Lasers & Ophthalmic Microscopes], Keratometers, Autorefractors, and Lensometers, Ophthalmic Ultrasound Systems & Digital Phoropters, Slit Lamps, Tonometers, Retinal Imaging Systems, General Examination Products, Chart Projectors, [Cataract & Cornea Examination Products, Specular Microscopes, Corneal Topography Systems, Wavefront Analyzers & Aberrometers, Optical Biometry Systems], Application (Cataract, Age-related Macular Degeneration, Glaucoma, Retinopathy, General Examination, Other Applications), End User (Hospitals, Clinics, Other End Users), and Geography. The study also evaluates industry competitors and analyzes their market shares at the country and regional levels.

Based on product type, in 2022, the retina & glaucoma examination products segment is expected to account for the largest share of the market. The large market share of this segment is attributed high penetration of retina examination products due to the high awareness of high-quality eye care and early and accurate diagnosis of common eye diseases such as macular degeneration, glaucoma, and diabetic retinopathy. The prevalence of diabetic retinopathy is rising globally, driving the demand for retina & glaucoma examination products.

Based on application, the optometry equipment market is segmented into cataract, age-related macular degeneration, glaucoma, retinopathy, general examination, and other applications. The general examination segment is projected to register the fastest growth rate over the forecast period. The growth of this segment is attributed to the growing geriatric population worldwide and the rising incidences of eye diseases primarily due to dependency on digital devices such as laptops, mobile phones, and others. General eye examinations help detect eye problems early when they can be treated most effectively. The awareness and importance of general eye examinations are high among all age groups, which is driving the growth of this market.

Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5406

Based on end user, in 2022, the clinics segment is expected to account for the largest share of the market. The large market share of this segment is attributed to factors such as a large number of private clinics in developed countries, patients’ preference for ophthalmic clinics for the diagnosis and treatment of eye diseases, and timely appointments at the ophthalmic clinics.

Geographic Review:

This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S. and Canada), Europe (Germany, France, U.K., Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa.

In 2022, North America is expected to account for the largest share of the optometry equipment market. In 2022, the U.S. is expected to account for the largest share of the optometry equipment market in North America. The U.S. has one of the most advanced healthcare systems globally. Availability of reimbursement policies, supportive initiatives for improving access to eye care services, and high awareness of eye care among the U.S. population are the key factors supporting the large share of the market.

Key Players

The key players operating in the global optometry equipment market are NIDEK CO. LTD. (Japan), Carl Zeiss Meditec AG (Germany), Alcon (U.S.), Heidelberg Engineering GmbH (Germany), Johnson & Johnson (U.S.), Canon, Inc. (Japan), Bausch Health Companies Inc. (Canada), Escalon Medical Corp (U.S.), Topcon Healthcare Solutions, Inc. (U.S.), and HEINE Optotechnik GmbH & Co. KG (Germany).

To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/optometry-equipment-market-5406

Key questions answered in the report-

Which are the high-growth market segments in terms of product type, application, end user, and region/country?

What was the historical market for optometry equipment across the globe?

What are the market forecasts and estimates for the period 2022–2029?

What are the major drivers, restraints, challenges, opportunities, and trends in the global market of optometry equipment?

Who are the major players in the global optometry equipment market?

How is the competitive landscape, and who are the market leaders in the global optometry equipment market?

What are the recent developments in the optometry equipment market?

What are the different strategies adopted by the major players in the optometry equipment market?

What are the geographical trends and high growth regions/countries?

Quick Buy- https://www.meticulousresearch.com/Checkout/36446863

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research

𝑹𝒆𝒗𝒐𝒍𝒖𝒕𝒊𝒐𝒏𝒊𝒛𝒊𝒏𝒈 𝑬𝒚𝒆 𝑪𝒂𝒓𝒆: 𝑻𝒉𝒆 𝑫𝒚𝒏𝒂𝒎𝒊𝒄 𝑳𝒂𝒏𝒅𝒔𝒄𝒂𝒑𝒆 𝒐𝒇 𝑶𝒑𝒕𝒐𝒎𝒆𝒕𝒓𝒚 𝑬𝒒𝒖𝒊𝒑𝒎𝒆𝒏𝒕 𝑴𝒂𝒓𝒌𝒆𝒕 Meticulous Research®—a leading global market research company, published a research report titled ‘Optometry Equipment Market by Product (OCT Scan, Perimeter, Fundus Camera, Retinoscope, Keratometer, Ophthalmic Ultrasound, Tonometer, Slit Lamp, Chart Projector), Application (Cataract, Glaucoma, AMD), End User (Clinic, Hospital) - Global Forecast to 2029.’ Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5406 According to this latest publication from Meticulous Research®, the global optometry equipment market is projected to reach $5.4 billion by 2029, at a CAGR of 4% during the forecast period. The increasing cases of eye diseases and disorders, rising geriatric population, excessive use of laptops & mobile phones leading to visual impairments, and rising government initiatives and funding to improve access to eye care services are the factors driving the growth of this market. Optometry Equipment Market: Future Outlook The global optometry equipment market is segmented by Product Type (Retina & Glaucoma Examination Products [OCT Scanners, Perimeters, Fundus Cameras, Retinoscopes, Ophthalmoscopes, Ophthalmic Lasers & Ophthalmic Microscopes], Keratometers, Autorefractors, and Lensometers, Ophthalmic Ultrasound Systems & Digital Phoropters, Slit Lamps, Tonometers, Retinal Imaging Systems, General Examination Products, Chart Projectors, [Cataract & Cornea Examination Products, Specular Microscopes, Corneal Topography Systems, Wavefront Analyzers & Aberrometers, Optical Biometry Systems], Application (Cataract, Age-related Macular Degeneration, Glaucoma, Retinopathy, General Examination, Other Applications), End User (Hospitals, Clinics, Other End Users), and Geography. The study also evaluates industry competitors and analyzes their market shares at the country and regional levels. Based on product type, in 2022, the retina & glaucoma examination products segment is expected to account for the largest share of the market. The large market share of this segment is attributed high penetration of retina examination products due to the high awareness of high-quality eye care and early and accurate diagnosis of common eye diseases such as macular degeneration, glaucoma, and diabetic retinopathy. The prevalence of diabetic retinopathy is rising globally, driving the demand for retina & glaucoma examination products. Based on application, the optometry equipment market is segmented into cataract, age-related macular degeneration, glaucoma, retinopathy, general examination, and other applications. The general examination segment is projected to register the fastest growth rate over the forecast period. The growth of this segment is attributed to the growing geriatric population worldwide and the rising incidences of eye diseases primarily due to dependency on digital devices such as laptops, mobile phones, and others. General eye examinations help detect eye problems early when they can be treated most effectively. The awareness and importance of general eye examinations are high among all age groups, which is driving the growth of this market. Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5406 Based on end user, in 2022, the clinics segment is expected to account for the largest share of the market. The large market share of this segment is attributed to factors such as a large number of private clinics in developed countries, patients’ preference for ophthalmic clinics for the diagnosis and treatment of eye diseases, and timely appointments at the ophthalmic clinics. Geographic Review: This research report analyzes major geographies and provides a comprehensive analysis of North America (U.S. and Canada), Europe (Germany, France, U.K., Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa. In 2022, North America is expected to account for the largest share of the optometry equipment market. In 2022, the U.S. is expected to account for the largest share of the optometry equipment market in North America. The U.S. has one of the most advanced healthcare systems globally. Availability of reimbursement policies, supportive initiatives for improving access to eye care services, and high awareness of eye care among the U.S. population are the key factors supporting the large share of the market. Key Players The key players operating in the global optometry equipment market are NIDEK CO. LTD. (Japan), Carl Zeiss Meditec AG (Germany), Alcon (U.S.), Heidelberg Engineering GmbH (Germany), Johnson & Johnson (U.S.), Canon, Inc. (Japan), Bausch Health Companies Inc. (Canada), Escalon Medical Corp (U.S.), Topcon Healthcare Solutions, Inc. (U.S.), and HEINE Optotechnik GmbH & Co. KG (Germany). To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/optometry-equipment-market-5406 Key questions answered in the report- Which are the high-growth market segments in terms of product type, application, end user, and region/country? What was the historical market for optometry equipment across the globe? What are the market forecasts and estimates for the period 2022–2029? What are the major drivers, restraints, challenges, opportunities, and trends in the global market of optometry equipment? Who are the major players in the global optometry equipment market? How is the competitive landscape, and who are the market leaders in the global optometry equipment market? What are the recent developments in the optometry equipment market? What are the different strategies adopted by the major players in the optometry equipment market? What are the geographical trends and high growth regions/countries? Quick Buy- https://www.meticulousresearch.com/Checkout/36446863 Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research0 Comments 0 Shares11 - 𝑫𝒊𝒈𝒊𝒕𝒂𝒍 𝑷𝒂𝒚𝒎𝒆𝒏𝒕 𝑴𝒂𝒓𝒌𝒆𝒕 𝑾𝒐𝒓𝒕𝒉 $274.61 𝑩𝒊𝒍𝒍𝒊𝒐𝒏 𝒃𝒚 2029

According to a new market research report titled, ‘Digital Payment Market by Offering (Solution & Services), Payment Mode (Digital Wallets, Banking Cards, POS, Internet Banking), End User (BFSI, Retail, Travel & Hospitality, Healthcare, Others), Organization Size and Geography - Global Forecasts to 2029,’ the digital payment market is projected to reach $274.61 billion by 2029, at a CAGR of 16.6% from 2022 to 2029.

Digital payments are transactions that take place via digital or online modes, with no physical exchange of money involved. This means that both parties, the payer and the payee, use electronic mediums to exchange money. Digital payment transactions have grown rapidly in emerging markets during the past two years as the pandemic accelerated shifts to contactless payments and e-commerce.

Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5410

The growth of this market is attributed to the increased adoption of digital payment modes, rising government initiatives for the adoption of digital payment and growing partnerships between banks and fintech to leverage customer experience. In addition, the increasing use of payment applications across different industry verticals and the rising adoption of contactless payment are expected to offer significant opportunities for the growth of this market. However, a low level of awareness of online payments in rural areas can restrain the growth of this market to some extent.

Digital payment firms such as PhonePe, Paytm, and Amazon Pay witnessed a nearly 50% spike in transactions through their digital wallets since the COVID-19 pandemic. The sudden increase in digital adoption dramatically advanced the digital transformation agendas for numerous banks, with banking leaders recognizing online banking services as a critical means for increasing customer retention and growing revenue streams through personalized services. The impact of the COVID-19 pandemic accelerated the adoption of a broad range of digital banking offerings and shifted consumers of all ages away from traditional banking branches and ATMs at an unprecedented pace.

The digital payment market is segmented based on offering (solutions and services), payment mode (digital wallets, banking cards, pos, and internet banking), end user (BFSI, retail, travel & hospitality, healthcare, and others), organization size, and geography. The study also evaluates industry competitors and analyses the market at the regional and country levels.

Based on offering, the digital payment market is segmented into solutions and services. In 2022, the solutions segment is expected to account for the largest share of the global digital payment market. The growth of the segment is attributed to the declining cash usage, the growing e-commerce industry, development in mobile payment technology, and increased use of mobile wallets.

Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5410

Based on payment mode, the digital payment market is segmented into digital wallets, banking cards, point of sales, internet banking, and other payment modes. In 2022, the digital wallets segment is expected to account for the largest share of the global digital payment market. Additionally, this segment is expected to grow at the highest CAGR during the forecast period. Factors such as increasing population, rising adoption of smartphones, rising number of internet subscribers, and rapid growth in the retail and e-commerce sector across the countries such as India and China are driving the market.

Based on end user, the digital payment market is segmented into BFSI, retail, travel and hospitality, healthcare, IT and telecom, media and entertainment, and others. In 2022, the BFSI segment is expected to account for the largest share of the global digital payment market. The rising demand for digital remittances for cross-border and domestic transactions is encouraging banks to adopt digital payment solutions. Moreover, banks are also enhancing their offerings to compete with digital payment solutions providers, such as Google, Amazon, and Facebook.

However, the retail segment is expected to grow with the highest CAGR during the forecasted period. Retail e-commerce sales are rapidly increasing due to government support, increased smartphone penetration, and application usage, and the promise of a better shopping experience is likely to boost. The increasing usage of mobile payments in the retail industry, primarily in the e-commerce sector, boosts the digital payment market in the retail sector.

Based on organization size, the digital payment market is segmented into large enterprises, small and medium-sized enterprises. In 2022, the large enterprises segment is expected to account for the largest share of the global digital payment market. Additionally, this segment is also expected to grow at the highest CAGR during the forecast period. The increasing number of high valuations transactions in large enterprises is compelling these enterprises to opt for premium digital payment solutions.

The report also includes an extensive assessment of the key growth strategies adopted by the leading market participants between 2020 and 2022. The key players operating in the digital payment market are PayPal Holdings, Inc. (U.S.), Fiserve, Inc. (U.S.), FIS (U.S.), Block, Inc., formerly Square, Inc. (U.S.), Stripe, Inc. (U.S.), Visa, Inc. (U.S.), Mastercard (U.S.), Worldline (France), Temenos (Switzerland), PayU (Netherlands), Apple Inc. (U.S.), JPMorgan Chase & Co. (U.S.), WEX Inc. (U.S.), ACI Worldwide, Inc. (U.S.), and FleetCor Technologies, Inc. (U.S.).

To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/digital-payment-market-5410

Scope of the report:

Digital Payment Market, by Offering

Solution

Services

Digital Payment Market, by Payment Mode

Digital Wallets

Banking Cards

Point of Sales

Internet Banking

Others Payment Modes

Digital Payment Market, by End User

BFSI

Retail

Travel and Hospitality

Healthcare

IT and Telecom

Media and Entertainment

Other End Users

Digital Payment Market, by Organization Size

Large Enterprises

Small and Medium-sized Enterprises

Digital payment Market, by Geography

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Quick Buy- https://www.meticulousresearch.com/Checkout/30539504

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research𝑫𝒊𝒈𝒊𝒕𝒂𝒍 𝑷𝒂𝒚𝒎𝒆𝒏𝒕 𝑴𝒂𝒓𝒌𝒆𝒕 𝑾𝒐𝒓𝒕𝒉 $274.61 𝑩𝒊𝒍𝒍𝒊𝒐𝒏 𝒃𝒚 2029 According to a new market research report titled, ‘Digital Payment Market by Offering (Solution & Services), Payment Mode (Digital Wallets, Banking Cards, POS, Internet Banking), End User (BFSI, Retail, Travel & Hospitality, Healthcare, Others), Organization Size and Geography - Global Forecasts to 2029,’ the digital payment market is projected to reach $274.61 billion by 2029, at a CAGR of 16.6% from 2022 to 2029. Digital payments are transactions that take place via digital or online modes, with no physical exchange of money involved. This means that both parties, the payer and the payee, use electronic mediums to exchange money. Digital payment transactions have grown rapidly in emerging markets during the past two years as the pandemic accelerated shifts to contactless payments and e-commerce. Download Free Report Sample Now @ https://www.meticulousresearch.com/download-sample-report/cp_id=5410 The growth of this market is attributed to the increased adoption of digital payment modes, rising government initiatives for the adoption of digital payment and growing partnerships between banks and fintech to leverage customer experience. In addition, the increasing use of payment applications across different industry verticals and the rising adoption of contactless payment are expected to offer significant opportunities for the growth of this market. However, a low level of awareness of online payments in rural areas can restrain the growth of this market to some extent. Digital payment firms such as PhonePe, Paytm, and Amazon Pay witnessed a nearly 50% spike in transactions through their digital wallets since the COVID-19 pandemic. The sudden increase in digital adoption dramatically advanced the digital transformation agendas for numerous banks, with banking leaders recognizing online banking services as a critical means for increasing customer retention and growing revenue streams through personalized services. The impact of the COVID-19 pandemic accelerated the adoption of a broad range of digital banking offerings and shifted consumers of all ages away from traditional banking branches and ATMs at an unprecedented pace. The digital payment market is segmented based on offering (solutions and services), payment mode (digital wallets, banking cards, pos, and internet banking), end user (BFSI, retail, travel & hospitality, healthcare, and others), organization size, and geography. The study also evaluates industry competitors and analyses the market at the regional and country levels. Based on offering, the digital payment market is segmented into solutions and services. In 2022, the solutions segment is expected to account for the largest share of the global digital payment market. The growth of the segment is attributed to the declining cash usage, the growing e-commerce industry, development in mobile payment technology, and increased use of mobile wallets. Speak to our Analysts: https://www.meticulousresearch.com/speak-to-analyst/cp_id=5410 Based on payment mode, the digital payment market is segmented into digital wallets, banking cards, point of sales, internet banking, and other payment modes. In 2022, the digital wallets segment is expected to account for the largest share of the global digital payment market. Additionally, this segment is expected to grow at the highest CAGR during the forecast period. Factors such as increasing population, rising adoption of smartphones, rising number of internet subscribers, and rapid growth in the retail and e-commerce sector across the countries such as India and China are driving the market. Based on end user, the digital payment market is segmented into BFSI, retail, travel and hospitality, healthcare, IT and telecom, media and entertainment, and others. In 2022, the BFSI segment is expected to account for the largest share of the global digital payment market. The rising demand for digital remittances for cross-border and domestic transactions is encouraging banks to adopt digital payment solutions. Moreover, banks are also enhancing their offerings to compete with digital payment solutions providers, such as Google, Amazon, and Facebook. However, the retail segment is expected to grow with the highest CAGR during the forecasted period. Retail e-commerce sales are rapidly increasing due to government support, increased smartphone penetration, and application usage, and the promise of a better shopping experience is likely to boost. The increasing usage of mobile payments in the retail industry, primarily in the e-commerce sector, boosts the digital payment market in the retail sector. Based on organization size, the digital payment market is segmented into large enterprises, small and medium-sized enterprises. In 2022, the large enterprises segment is expected to account for the largest share of the global digital payment market. Additionally, this segment is also expected to grow at the highest CAGR during the forecast period. The increasing number of high valuations transactions in large enterprises is compelling these enterprises to opt for premium digital payment solutions. The report also includes an extensive assessment of the key growth strategies adopted by the leading market participants between 2020 and 2022. The key players operating in the digital payment market are PayPal Holdings, Inc. (U.S.), Fiserve, Inc. (U.S.), FIS (U.S.), Block, Inc., formerly Square, Inc. (U.S.), Stripe, Inc. (U.S.), Visa, Inc. (U.S.), Mastercard (U.S.), Worldline (France), Temenos (Switzerland), PayU (Netherlands), Apple Inc. (U.S.), JPMorgan Chase & Co. (U.S.), WEX Inc. (U.S.), ACI Worldwide, Inc. (U.S.), and FleetCor Technologies, Inc. (U.S.). To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/digital-payment-market-5410 Scope of the report: Digital Payment Market, by Offering Solution Services Digital Payment Market, by Payment Mode Digital Wallets Banking Cards Point of Sales Internet Banking Others Payment Modes Digital Payment Market, by End User BFSI Retail Travel and Hospitality Healthcare IT and Telecom Media and Entertainment Other End Users Digital Payment Market, by Organization Size Large Enterprises Small and Medium-sized Enterprises Digital payment Market, by Geography North America Europe Asia-Pacific Latin America Middle East & Africa Quick Buy- https://www.meticulousresearch.com/Checkout/30539504 Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research0 Comments 0 Shares11 - 𝑩𝒖𝒊𝒍𝒅𝒊𝒏𝒈 𝒕𝒉𝒆 𝑭𝒖𝒕𝒖𝒓𝒆- 𝑻𝒉𝒆 𝑺𝒖𝒓𝒈𝒊𝒏𝒈 𝑫𝒆𝒎𝒂𝒏𝒅 𝒇𝒐𝒓 𝑨𝒅𝒗𝒂𝒏𝒄𝒆𝒅 3𝑫 𝑷𝒓𝒊𝒏𝒕𝒊𝒏𝒈 𝑴𝒂𝒕𝒆𝒓𝒊𝒂𝒍𝒔

Meticulous Research®— a leading global market research company, published a research report titled “3D Printing Materials Market by Type (Polymer, Metal, Ceramics & Composites), Form (Filament, Liquid, Powder), Technology (FDM, SLA, Polyjet, Multijet, Binder Jetting, EBM), Application - Global Forecast to 2028”.

With the use of 3D printing technologies, the prototypes are produced with much faster speed and with more durability. Prototyping is one of the primary application areas for 3D printing. Amongst the different 3D printing materials, polymer is the most widely used material. Polymers are used to fabricate high-tech industrial (aerospace, medical/dental, automotive, electronic), consumer (home, fashion, and entertainment) products. Advancements in polymeric materials continue to offer new possibilities for the manufacturing industry. The recycling and reuse of polymer 3D printing materials have encouraged many industries to adopt additive manufacturing (AM) in-house.

Download Free Research Sample @ https://www.meticulousresearch.com/download-sample-report/cp_id=5083

3D printing or additive manufacturing is a process of manufacturing three dimensional solid objects from a digital file. 3D printing technology creates an object by laying down successive layers of material until the object is created.

Each of these layers can be seen as a thinly sliced cross-section of the object. 3D printing technology refers to a variety of processes in which material is deposited, joined, or solidified with computer control to create a three-dimensional object.

The major factors driving the 3D printing materials market include growing demand for polymers in 3D printing, mass customization of various functional parts for industrial equipment, jewellery, and consumer goods, and government initiatives to support the adoption of 3D printing.

Lack of awareness of 3D printing technology among supplies, buyers, users, and lack of skilled laborers to perform 3D printing operations is a major challenge for the growth of the 3D printing materials market.

Governments around the world are also supporting the adoption of 3D printing through various initiatives, including funding for research and development and tax incentives for companies that use 3D printing in their operations.

Speak to our Analysts- https://www.meticulousresearch.com/speak-to-analyst/cp_id=5083

However, the lack of awareness of 3D printing technology among suppliers, buyers, and users, as well as the shortage of skilled laborers to perform 3D printing operations, are significant challenges for the growth of the 3D printing materials market. Despite these challenges, the future looks bright for this exciting technology.

The key players operating in the global 3D printing materials market are 3D Systems Corporation (U.S.), Proto Labs, Ltd., (U.S.), The ExOne Company (U.S.), HP INC. (U.S.), EnvisionTEC, Inc. (U.S.), Markforged, Inc. (U.S.), Tethon 3D (U.S.), Evonik Industries AG (Germany), Materialise NV (Belgium), EOS GmbH (Germany), Stratasys Ltd. (Israel), Zortrax (Poland), Sculpteo (France), Lithoz GmbH (Austria), and IC3D, LLC. (U.S.) among others.

To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/3d-printing-materials-market-5083

Key Questions Answered in the Report-

Which are the high-growth market segments in terms of type, form, technology, application, and geography?

What is the historical market size for 3D printing materials across the globe?

What are the market forecasts and estimates for the period 2021-2028?

What are the major drivers, restraints, opportunities, and challenges in the 3D printing materials market?

Who are the major players in the market, and what are their market shares?

Who are the major players in various countries?

How is the competitive landscape for the 3D printing materials market?

What are the recent developments in the 3D printing materials market?

Quick Buy : https://www.meticulousresearch.com/Checkout/27404287

Contact Us:

Meticulous Research®

Email- [email protected]

Contact Sales- +1-646-781-8004

Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research𝑩𝒖𝒊𝒍𝒅𝒊𝒏𝒈 𝒕𝒉𝒆 𝑭𝒖𝒕𝒖𝒓𝒆- 𝑻𝒉𝒆 𝑺𝒖𝒓𝒈𝒊𝒏𝒈 𝑫𝒆𝒎𝒂𝒏𝒅 𝒇𝒐𝒓 𝑨𝒅𝒗𝒂𝒏𝒄𝒆𝒅 3𝑫 𝑷𝒓𝒊𝒏𝒕𝒊𝒏𝒈 𝑴𝒂𝒕𝒆𝒓𝒊𝒂𝒍𝒔 Meticulous Research®— a leading global market research company, published a research report titled “3D Printing Materials Market by Type (Polymer, Metal, Ceramics & Composites), Form (Filament, Liquid, Powder), Technology (FDM, SLA, Polyjet, Multijet, Binder Jetting, EBM), Application - Global Forecast to 2028”. With the use of 3D printing technologies, the prototypes are produced with much faster speed and with more durability. Prototyping is one of the primary application areas for 3D printing. Amongst the different 3D printing materials, polymer is the most widely used material. Polymers are used to fabricate high-tech industrial (aerospace, medical/dental, automotive, electronic), consumer (home, fashion, and entertainment) products. Advancements in polymeric materials continue to offer new possibilities for the manufacturing industry. The recycling and reuse of polymer 3D printing materials have encouraged many industries to adopt additive manufacturing (AM) in-house. Download Free Research Sample @ https://www.meticulousresearch.com/download-sample-report/cp_id=5083 3D printing or additive manufacturing is a process of manufacturing three dimensional solid objects from a digital file. 3D printing technology creates an object by laying down successive layers of material until the object is created. Each of these layers can be seen as a thinly sliced cross-section of the object. 3D printing technology refers to a variety of processes in which material is deposited, joined, or solidified with computer control to create a three-dimensional object. The major factors driving the 3D printing materials market include growing demand for polymers in 3D printing, mass customization of various functional parts for industrial equipment, jewellery, and consumer goods, and government initiatives to support the adoption of 3D printing. Lack of awareness of 3D printing technology among supplies, buyers, users, and lack of skilled laborers to perform 3D printing operations is a major challenge for the growth of the 3D printing materials market. Governments around the world are also supporting the adoption of 3D printing through various initiatives, including funding for research and development and tax incentives for companies that use 3D printing in their operations. Speak to our Analysts- https://www.meticulousresearch.com/speak-to-analyst/cp_id=5083 However, the lack of awareness of 3D printing technology among suppliers, buyers, and users, as well as the shortage of skilled laborers to perform 3D printing operations, are significant challenges for the growth of the 3D printing materials market. Despite these challenges, the future looks bright for this exciting technology. The key players operating in the global 3D printing materials market are 3D Systems Corporation (U.S.), Proto Labs, Ltd., (U.S.), The ExOne Company (U.S.), HP INC. (U.S.), EnvisionTEC, Inc. (U.S.), Markforged, Inc. (U.S.), Tethon 3D (U.S.), Evonik Industries AG (Germany), Materialise NV (Belgium), EOS GmbH (Germany), Stratasys Ltd. (Israel), Zortrax (Poland), Sculpteo (France), Lithoz GmbH (Austria), and IC3D, LLC. (U.S.) among others. To gain more insights into the market with a detailed table of content and figures, click here: https://www.meticulousresearch.com/product/3d-printing-materials-market-5083 Key Questions Answered in the Report- Which are the high-growth market segments in terms of type, form, technology, application, and geography? What is the historical market size for 3D printing materials across the globe? What are the market forecasts and estimates for the period 2021-2028? What are the major drivers, restraints, opportunities, and challenges in the 3D printing materials market? Who are the major players in the market, and what are their market shares? Who are the major players in various countries? How is the competitive landscape for the 3D printing materials market? What are the recent developments in the 3D printing materials market? Quick Buy : https://www.meticulousresearch.com/Checkout/27404287 Contact Us: Meticulous Research® Email- [email protected] Contact Sales- +1-646-781-8004 Connect with us on LinkedIn- https://www.linkedin.com/company/meticulous-research0 Comments 0 Shares11

More Stories